{kind=link}

Vietnam’s Expanding Industrial Park Landscape

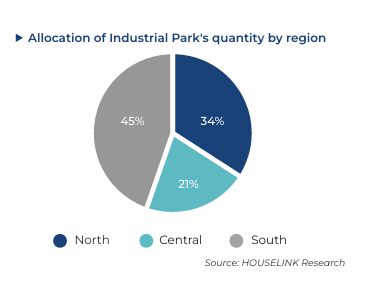

Vietnam is witnessing a remarkable surge in industrial development, characterized by the establishment of approximately 429 operating industrial parks. These parks boast a sprawling total planned industrial land area of about 142,162 hectares, primarily concentrated in the Northern and Southern regions. This growth reflects the nation’s strategic positioning as an industrial hub in Southeast Asia.

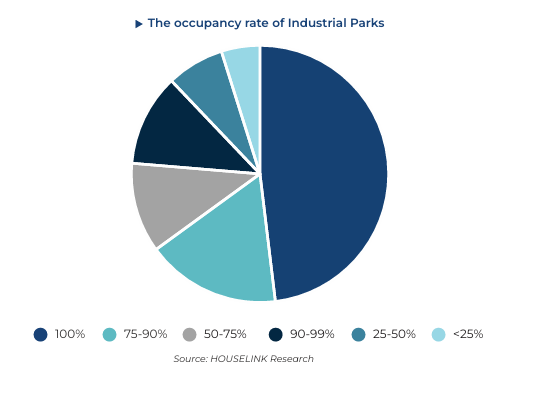

Based on a detailed survey of 267 operating industrial parks, the average occupancy rate is around 80%. Notably, 48% of these parks are fully occupied, while 28% boast an occupancy rate above 75%. This highlights not only the demand for industrial space but also the significant role these parks play in attracting and retaining businesses in Vietnam.

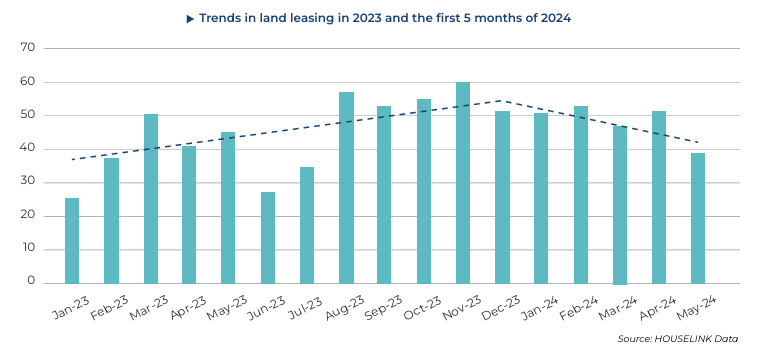

Interestingly, data from the HOUSELINK system reveals a fluctuating absorption rate of industrial land. Initially, the beginning of 2024 witnessed a remarkable absorption growth rate exceeding 70% compared to the prior year. However, by April and May, a decline was noted, with the absorbed industrial land area in May totaling 124.4 hectares—a 55% dip from May 2023. Nevertheless, the overall absorption from January to May 2024 exceeded the previous year’s figures by 12%, indicating ongoing resilience in the industrial sector.

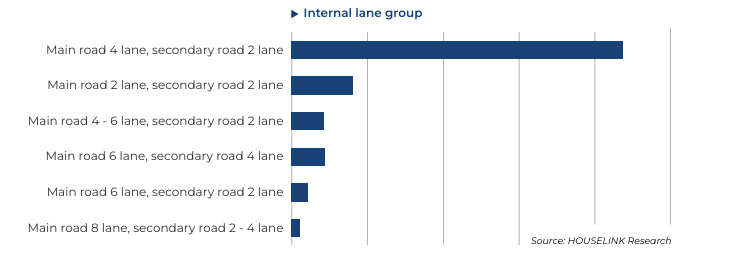

On the infrastructure front, a survey of internal transportation networks within industrial parks indicates significant compliance with standard design criteria. Most parks are equipped with main roads featuring 4 lanes and secondary roads with 2 lanes, facilitating efficient logistics and operations. This infrastructure sets a solid foundation for industrial growth and operational efficiency.

Transport connectivity remains a vital advantage for domestic industrial parks, with a substantial 67% situated adjacent to national highways. These highways are essential trade routes that enhance the logistics capabilities for businesses operating within these parks. Additionally, the ongoing improvement of the highway system, including the development of North-South expressways and coastal roads, is pivotal for overall economic advancement across the provinces and cities connected by these routes.

Power supply is the lifeblood of any industrial operation, and currently, most parks rely on the national grid. However, there’s a notable trend toward incorporating renewable energy sources, with nearly 50% implementing rooftop solar power systems. This shift reflects a broader commitment to sustainability and green production standards, aligning with global movements toward environmentally friendly industrial practices.

The proximity of industrial parks to residential areas further enhances their attractiveness to both investors and potential laborers. Areas such as Bac Ninh, Binh Duong, Dong Nai, Hanoi, and Ho Chi Minh City have nearly all industrial parks located close to residential communities, facilitating easy access for workforce commuting.

Moreover, infrastructure facilities surrounding these parks are rapidly developing. Services like supermarkets, hospitals, customs offices, and fire departments are increasingly integrated within or near these industrial zones, ensuring a higher quality of life for workers and improving operational efficiency for businesses.

Trends in Industrial Real Estate Rental Prices

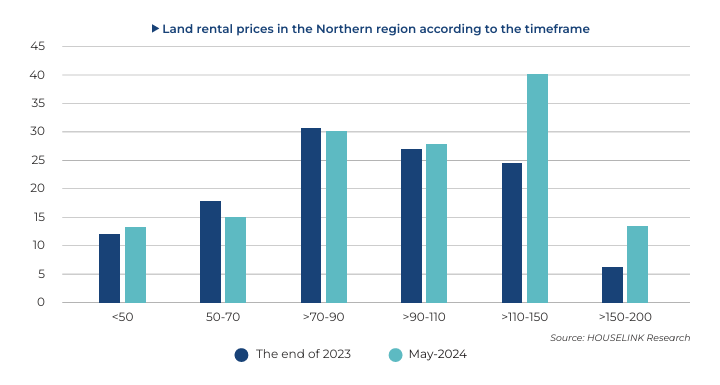

A recent survey indicates a clear trend in the rental prices for industrial real estate in 2024 compared to the end of 2023. The second quarter of 2024 sees a distinct shift, particularly in higher rental ranges. While the rental price band of ≤50 USD/m2/lease term decreased by 7%, the rental range of >150-200 USD/m2/lease term increased by 4%. This indicates a shifting market where demand drives prices upward at the higher end of the scale.

For ready-built factory (RBF) spaces, slight price fluctuations have occurred, particularly in the ranges of 2-3 USD/m2/month and >5 USD/m2/month. Interestingly, while the majority of industrial parks maintain rental prices between 3-5 USD/m2/month, the segment above 5 USD/m2/month has seen a decrease of 2%, likely reflecting market adjustments amidst increasing competition.

Forecasts for GDP growth in Vietnam place it at 5.3% for the second quarter of 2024, down from previous expectations. Inflationary pressures remain a concern, with the Consumer Price Index (CPI) averaging an increase of 4.03% in early 2024. Despite these economic challenges, the overall Industrial Production Index (IIP) has risen by 6.8%, signaling underlying strength within the industrial sector.

Export and import values have rebounded, achieving their highest levels since 2020. Exports reached $156.8 billion, up 15.2%, while imports hit $149.8 billion, up 18.2%. This solid trade performance, coupled with a trade surplus of $8 billion, underscores Vietnam’s robust positioning in the global marketplace.

Investment Attraction in Industrial Parks

The first half of 2024 has shown encouraging trends in attracting investment projects. The quantity of projects has increased significantly compared to previous years, reflecting a strong recovery from the pandemic’s impact. The number of investment projects rose by 11% compared to the same period in 2019, showcasing Vietnam’s resilience and growing appeal to both domestic and foreign investors.

Among the countries investing in Vietnam, China leads in project numbers, followed closely by Hong Kong, Taiwan, South Korea, and Singapore. Notably, while Hong Kong ranks second in project quantity, it features a lower total investment amount, whereas South Korea’s investments are substantial despite a lower project count.

The shift in preference towards leasing factories rather than land is evident, driven by investors aiming to commence operations quickly. As legal restrictions and rising rental costs inhibit land availability, many investors prioritize factory leasing to expedite their entry into the market.

Contrary to the upward trend in factory leasing, the proportion of projects leasing land has seen a decrease. Rising land rental prices in key provinces and limited land supply are primary concerns for investors, influencing this trend.

Throughout the past three years, investment-attractive regions have predominantly been in the northern and southern areas of Vietnam. Provinces such as Bac Ninh, Binh Duong, Long An, Dong Nai, and Hai Phong have established comprehensive industrial complexes that effectively integrate manufacturing and support industries, leading the charge in attracting considerable investment.

Here you can access reports on Vietnam’s construction market and industry investments.

Please sign up to receive periodic reports by filling up the form below.

Source: HOUSELINK