{kind=link}

By

Knight Frank

Tue, February 18, 2025 | 8:00 am GMT+7

Vietnam’s real estate market saw a remarkable performance in 2024, spanning the office, ready-built factories and warehouses, and apartment segments. Analysts from Knight Frank have highlighted this growth, attributing it to strong market fundamentals.

A property project built by Hoa Binh Construction Group. Photo courtesy of Thanh Nien (Young People) newspaper.

In 2025, Vietnam is positioned as one of the top three emerging markets in the region, alongside India and Indonesia, especially in terms of industrial and investment growth.

The strong potential for foreign direct investment (FDI) is fundamentally supported by Vietnam’s strategic location, favorable demographics, and open economic policies. These elements have cooperatively enhanced the performance of Vietnam’s property market, particularly in 2024.

Office Market Insights

Vietnam’s office market experienced significant growth in 2024, with net absorption surpassing 160,000 square meters—the highest in five years. This surge was driven by rapid expansion within the IT, technology, and finance sectors. Notably, there was a predominant trend of “flight to quality,” with new, green-certified buildings in Ho Chi Minh City and Hanoi securing large-scale transactions.

In Ho Chi Minh City, over 118,000 square meters of new office space was introduced, primarily in prime locations such as District 1, featuring projects like The Nexus, Riverfront Financial Centre, ThaiSquare The Merit, and e.town 6 in Tan Binh district.

Similarly, Hanoi saw nearly 87,000 square meters of new space coming online, attracting strong pre-lease interest due to high construction quality and competitive leasing terms. While average asking rents remained elevated across both cities, landlords began offering flexible policies, including rent-free periods and discounts on longer lease agreements.

Ready-Built Factories and Warehouses

Vietnam’s strategic geographical position and cost-effectiveness have established it as an essential “China-plus-one” destination, particularly since the onset of the U.S.-China trade war in 2018. Over the past six years, the ready-built factory and warehouse (RBF/RBW) market has doubled its supply from 6.6 million square meters in 2018 to over 15.6 million square meters by 2024, largely driven by institutional developers like BW, SLP, and Frasers.

Prominent industrial hubs have been established in Bac Ninh and Hai Phong, with notable new projects generating significant supply, such as BW Thuan Thanh 3B and BW ESR Nam Dinh Vu. In the Southern region, industrial parks in Dong Nai and Long An continue to attract investors, highlighted by projects such as KCN Ho Nai and BW Xuyen A.

Occupancy rates remained robust, averaging above 80% across both regions, thanks in part to the expansion of e-commerce and manufacturing flows from SMEs based in China and Europe. Moving forward, properties compliant with ESG standards and hybrid offerings are anticipated to gain traction, with Tier-2 markets like Ha Nam and Bac Giang projected to flourish.

Apartment Market Overview

The apartment market in Hanoi boomed during 2024, witnessing the launch of 27,268 new units, effectively tripling the supply seen in 2023. The West (Nam Tu Liem district) and East (Gia Lam district) of Hanoi emerged as key contributors, with township projects comprising over 80% of new supply.

In contrast, the Ho Chi Minh City market faced challenges, including tightened credit controls and ongoing legal struggles, leading to only 4,888 new units being launched—a 58% decline from the previous year. Within the HCMC market, Thu Duc City (located in the East) accounted for over 2,400 of these new units.

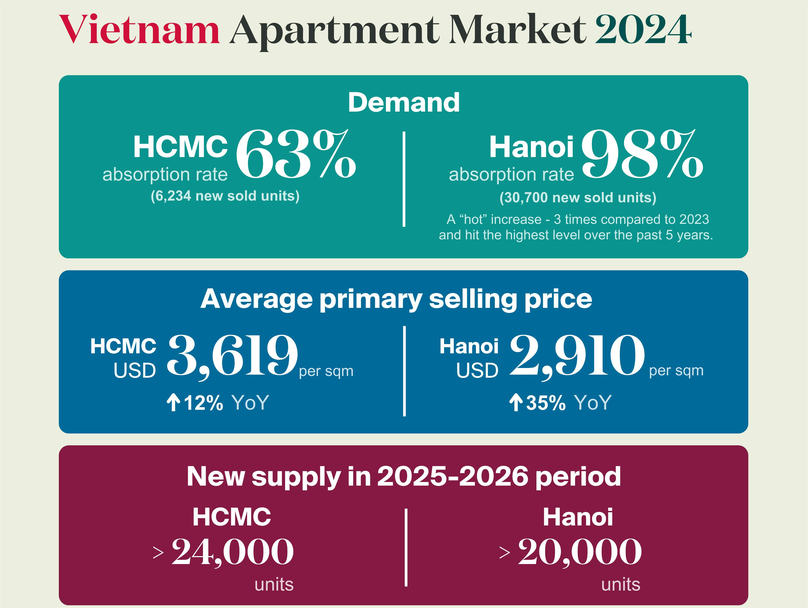

After a low demand phase in 2023, HCMC’s apartment market showed signs of recovery, with an absorption rate of 63%, translating to 6,234 units sold. The strongest sales activity occurred in Thu Duc City, which represented 67% of total sales.

Hanoi’s apartment demand, on the other hand, surged dramatically, achieving a 98% absorption rate with over 30,700 units sold—three times the volume recorded in 2023 and the highest over the last five years. Township projects in West and East Hanoi dictated demand, correlating to their significant contributions in sales volume.

In terms of pricing, HCMC’s average primary price was around $3,619 per square meter—up 12% year-over-year—while Hanoi saw its average price converge, increasing by 35% to reach $2,910 per square meter.

Looking ahead, HCMC is expected to introduce over 24,000 units in the 2025-2026 timeframe, with nearly 8,600 units anticipated in 2025 and 15,400 in 2026. Hanoi too aims for over 20,000 units annually, primarily driven by township projects.

“Integrated townships are redefining modern living, combining international-quality housing with a wealth of amenities. These townships significantly influenced the market in 2024 and are set to constitute nearly half of the city’s future supply over the next 5-7 years,” expressed Son Hoang, a valuation and advisory associate director at Knight Frank Vietnam.

(function(d, s, id) {

var js, fjs = d.getElementsByTagName(s)[0];

if (d.getElementById(id)) return;

js = document.createElement(s); js.id = id;

js.src = “//connect.facebook.net/vi_en/sdk.js#xfbml=1&version=v13.0&appId=3168341520106228”;

fjs.parentNode.insertBefore(js, fjs);

}(document, ‘script’, ‘facebook-jssdk’));