{kind=link}

Chinese FDI in Global Context

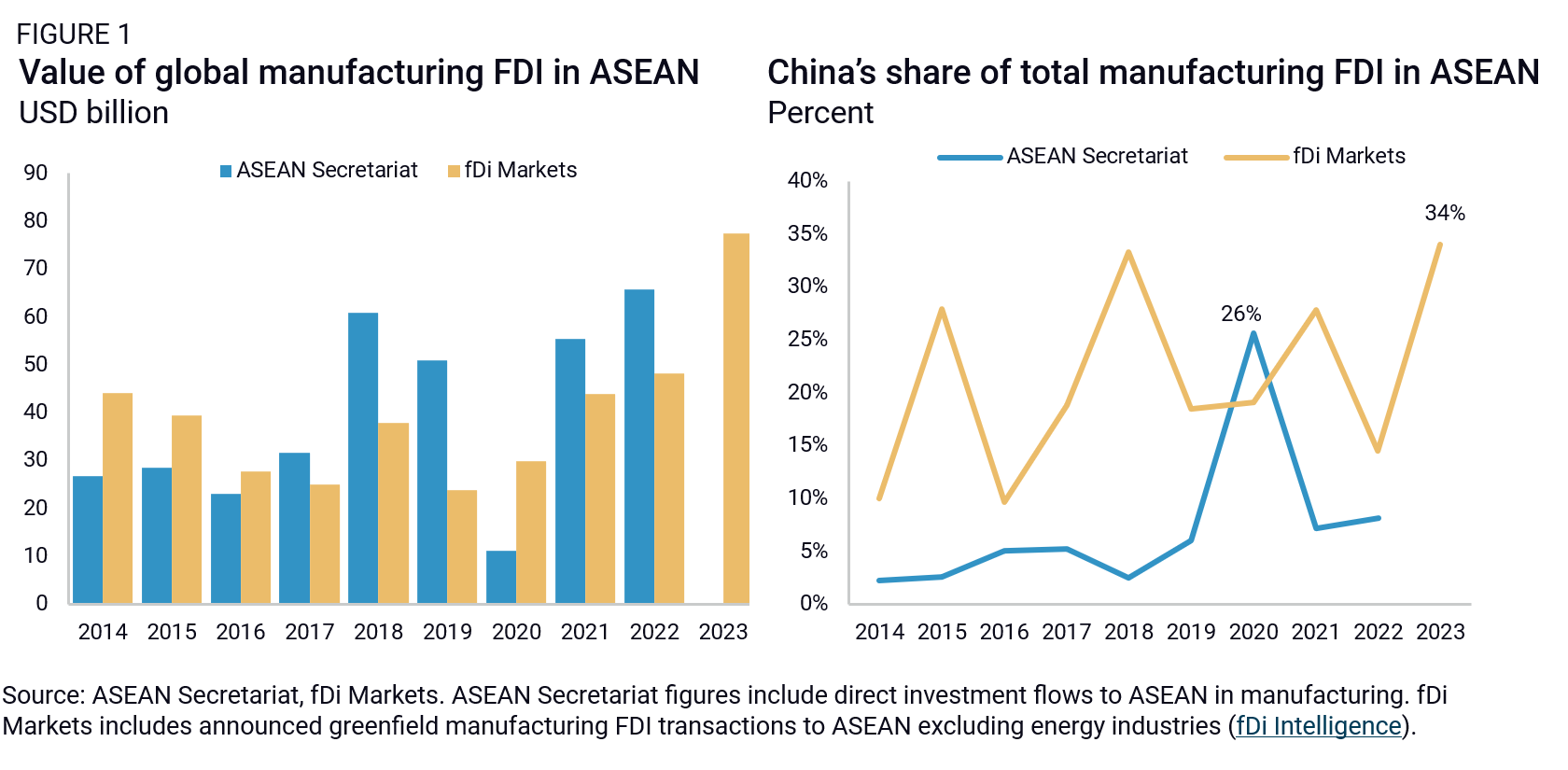

Since 2017, global manufacturing investment in the ten countries of ASEAN (the Association of Southeast Asian Nations) has surged significantly. Data from ASEAN indicates that foreign direct investment (FDI) in the region averaged around $30 billion annually from 2013 to 2017, but this figure skyrocketed to $60.8 billion in 2018. Excluding the dramatic decline caused by COVID-19 in 2020, the average annual FDI from 2018 to 2022 remained robust at $58 billion, with a 61% increase noted in 2023 compared to the previous year.

The remarkable FDI growth in 2018 was largely a response to the escalating U.S.-China trade tensions that began with the first trade war in 2017, combined with the strong economic growth rates within ASEAN’s principal markets. Interestingly, during this same period, greenfield FDI in China saw a sharp decline. Factors such as COVID-19 related disruptions to supply chains and the continuing U.S.-China rivalry, characterized by de-risking policies introduced under the Biden administration, led firms to diversify their operational bases away from China.

Chinese companies have played a significant role in this FDI surge, although estimates of their contributions vary across datasets. According to official ASEAN data, American firms are the dominant investors in the region, accounting for 25% of total manufacturing FDI from 2018 to 2022, followed by Japan at 11% and the EU at 10%. China’s stake grew rapidly but remains at around 8% in this context. In contrast, fDi Markets estimates China’s contribution to be much higher, at roughly 25%.

A closer look suggests that the actual contributions from Chinese enterprises may be even larger. The figures from the ASEAN Secretariat do not capture the investment routed through holding companies and offshore vehicles, which are prevalent in Chinese FDI, particularly via Hong Kong. Moreover, significant flows of Chinese capital to ASEAN occur through Singapore, as illustrated by Vietnam’s 2023 data, which showed that Singapore and Hong Kong together accounted for 31% of FDI inflows, whereas only 12% was directly attributed to China.

Breaking Down China’s Manufacturing FDI in ASEAN

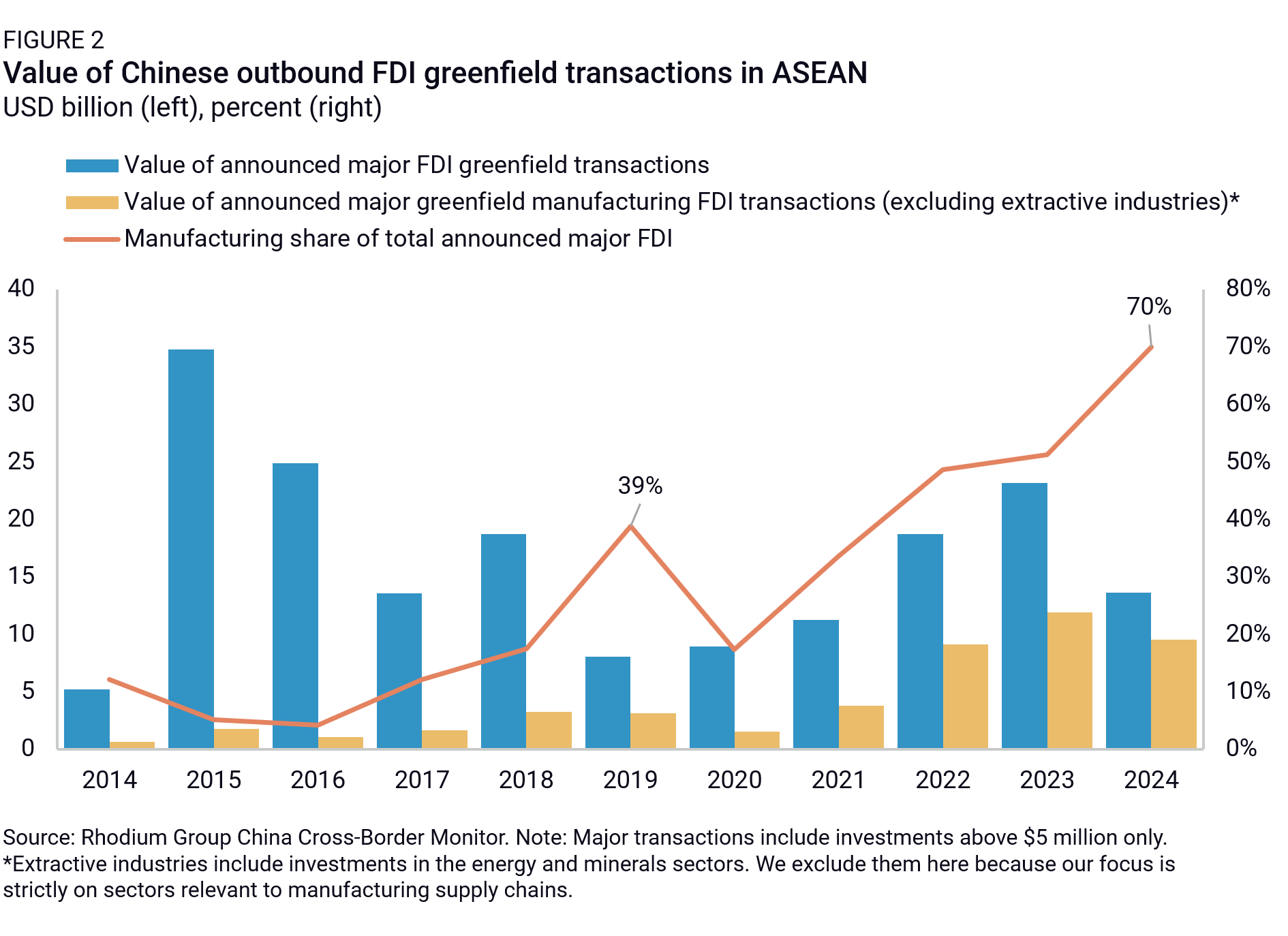

The Rhodium Group’s China Cross-Border Monitor (CBM) database, tracking verified investment transactions, provides valuable insights into Chinese FDI within ASEAN’s manufacturing sector. This granular approach reveals shifts in investor sentiment as they arise, bypassing potential distortions inherent in official statistics. The CBM allows for further breakdown by economies, sectors, and investment types, encompassing both mergers and acquisitions (M&A) and greenfield investments.

From 2010 to 2017, Chinese greenfield manufacturing FDI into ASEAN grew steadily, propelled by robust GDP growth and increasing operational costs in China. The geographic and cultural proximity between China and ASEAN, accompanied by trade integration under the ASEAN-China Free Trade Area, facilitated this trend.

However, in 2018, the landscape changed dramatically as manufacturing FDI nearly doubled year-over-year in response to the initial wave of U.S. tariffs on Chinese exports. From 2018 to 2021, FDI levels remained elevated, approximately three times higher than the average from 2014 to 2017. This trend continued with a notable uptick starting in 2022 after China lifted its zero-COVID restrictions, pushing FDI levels to an average of $10 billion over the past three years—compared to $2.7 billion in the previous five years.

Historically, four countries have attracted the majority of Chinese investments: Indonesia and Vietnam, which together accounted for about 56% of total value from 2018 to 2024; Thailand at 18%; and Malaysia at 14%. Recently, Indonesia has expanded its lead, constituting 30% of total FDI value over the past three years, chiefly due to capital-intensive projects in the electric vehicle industry. However, the significance of Thailand, Vietnam, and Malaysia remains high, as they collectively accounted for 77% of transaction counts in the same period.

Some nations have seen less interest. While Singapore captured some manufacturing attention, especially in high-tech sectors like pharmaceuticals, it mainly serves as a hub for M&A and Chinese business services rather than manufacturing investments. Meanwhile, the Philippines and Brunei have been largely overlooked, attracting more investment in energy and raw material processing than in manufacturing. Finally, Myanmar, Laos, and Cambodia lag in attracting substantial investment figures, although Cambodia has seen a doubling in the number of major Chinese manufacturing transactions in recent years.

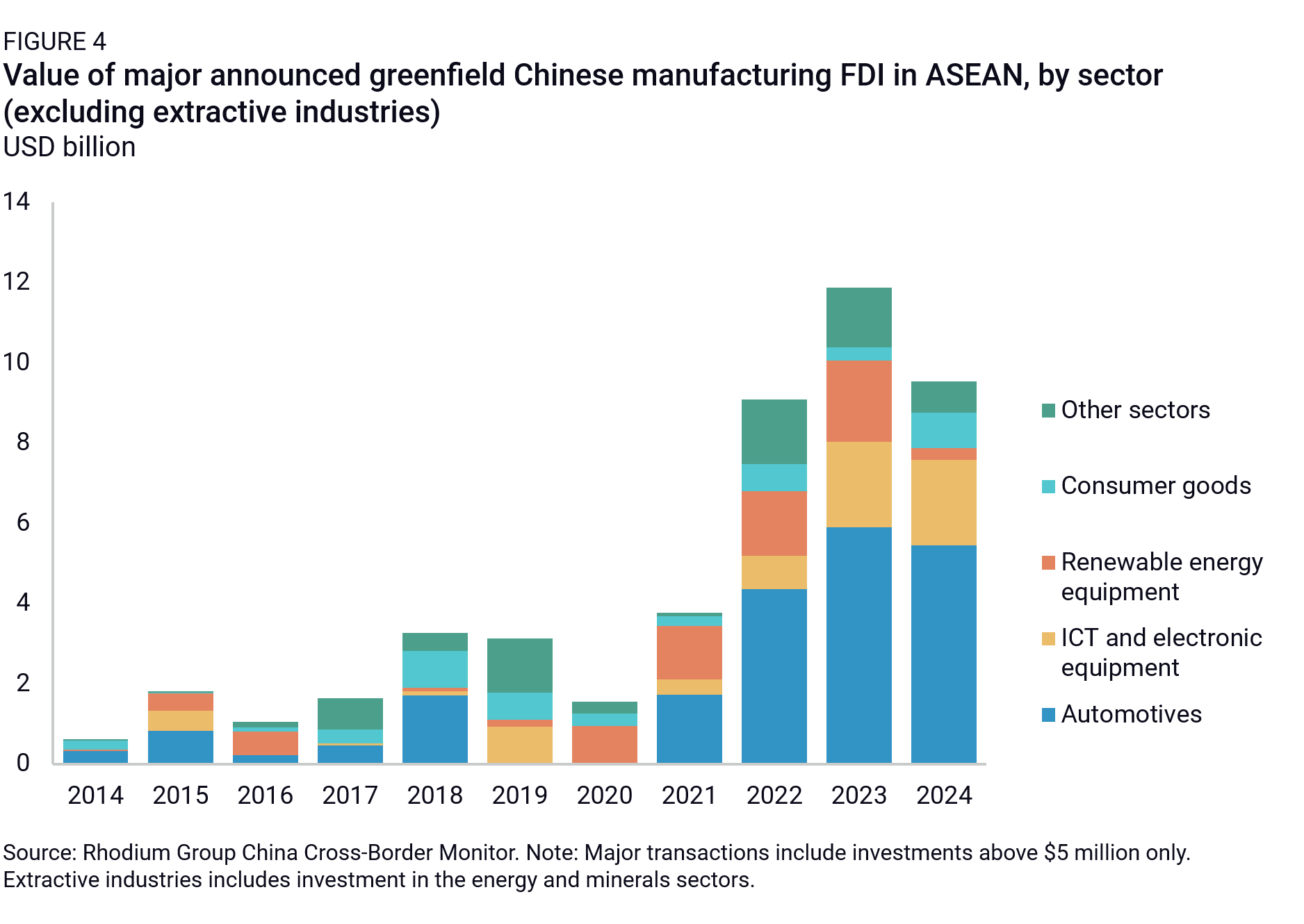

Over the past seven years, four key sectors have dominated China’s FDI into ASEAN countries, representing over 86% of total investment value. These include the automotive sector (45% of total FDI since 2018), ICT and electronics (15%), renewable energy equipment (15%), and consumer goods (9%). Analysis of these sectors helps elucidate the driving forces behind China’s manufacturing expansion into ASEAN.

Consumer Goods

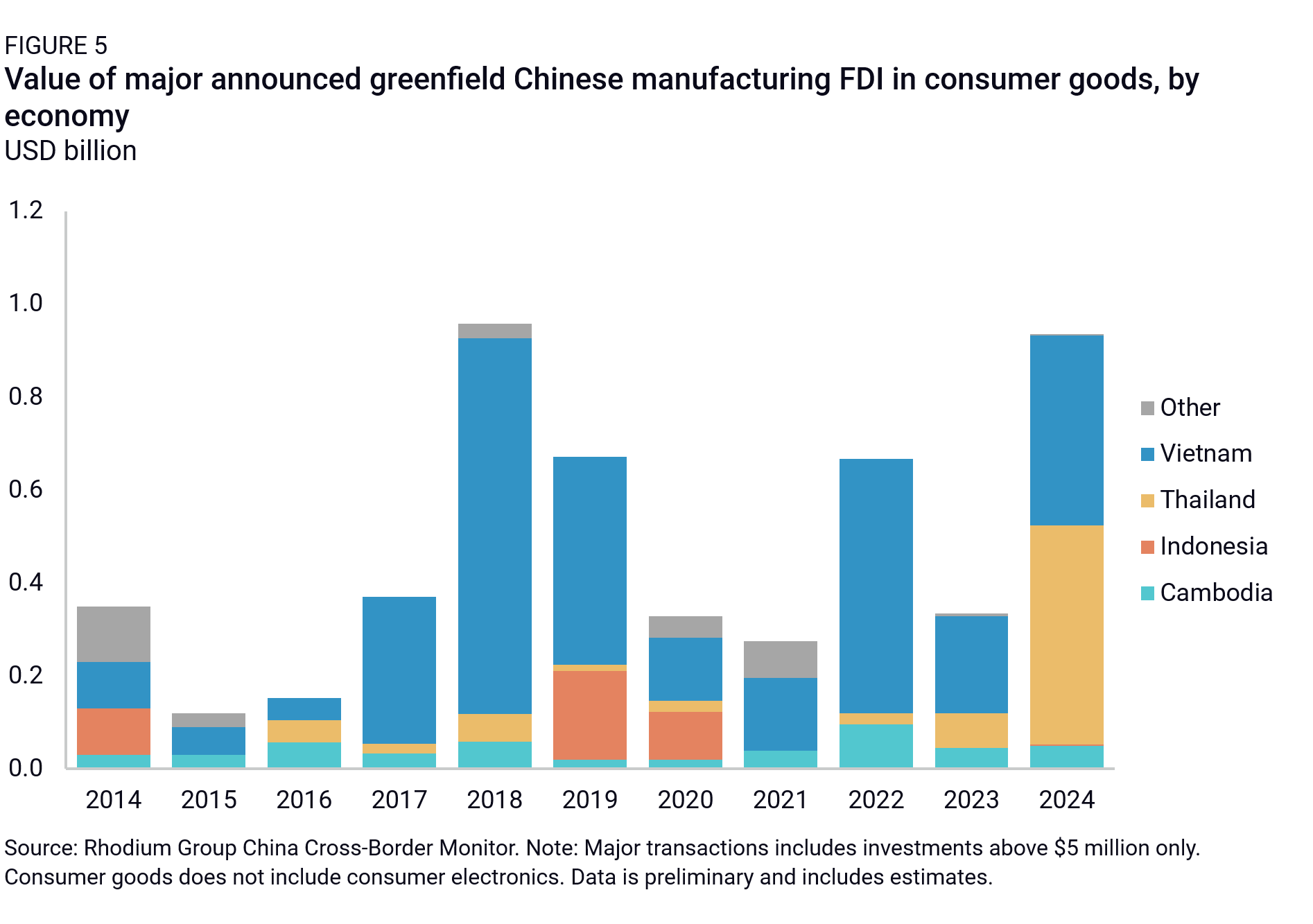

Chinese manufacturing of consumer goods, including textiles and furniture, was among the first to migrate offshore due to rising domestic wage levels, making Southeast Asia an attractive destination. The region’s cost advantages, logistical convenience, and favorable trade agreements have made it a primary target. Since the mid-2010s, investment rates have surged, with Vietnam capturing nearly two-thirds of announced Chinese greenfield projects in this space. This dominance is bolstered by Vietnam’s positioning within global supply chains and its preferential access to U.S. and EU markets.

This initial wave of investment was primarily driven by structural considerations concerning cost and capacity limitations. However, the U.S.-China trade war ushered in a more reactive phase of manufacturing FDI. For instance, businesses involved in household appliances, subjected to tariffs up to 25%, started relocating final assembly to Southeast Asia—especially Vietnam, Cambodia, and Indonesia. Investment figures in these sectors rose from an average of $240 million annually between 2014 and 2017 to $560 million per year from 2018 to 2021. A portion of these flows also targeted local consumer demand, as evidenced by significant investments in e-commerce firms like Alibaba’s involvement in Lazada and Tokopedia.

Post-pandemic, the rationale for offshore manufacturing by China remains intact but has evolved into a more strategic long-term approach. Investment activity surged, peaking at $935 million in 2024, with a heightened focus on higher-value segments. Thailand has emerged as increasingly popular for home appliance production, while businesses continue to explore lower-capital, labor-intensive opportunities in nations like Cambodia.

ICT and Electronics

The shift of Chinese electronics manufacturing offshore began in the mid-2010s yet gained significant momentum post-U.S.-China trade war. Investment levels virtually doubled after 2017 and saw another spike after COVID-19, especially from 2023 onward. Although electronics benefited from tariff exemptions during the trade conflicts, major Western tech firms sought to reduce reliance on China, exploring new growth markets while navigating intense local competition.

In the semiconductor sector, key players like JCET, TongFu Microelectronics, and Yangzhou Yangjie Electronics have set up operations in ASEAN to offer outsourced assembly and testing services, predominantly in Malaysia, which captured about 67% of regional investment in this field. In consumer electronics, Vietnam emerged as the regional hub, attracting an impressive 85% of industry investments between 2018 and 2024. Major Chinese suppliers of IT components for companies like Apple and LG also expanded their operations in response to the changing landscape.

After the pandemic, Chinese investments in intermediary components surged to meet increasing demands across various sectors. By 2024, these components accounted for 72% of newly announced investments in ICT and electronics. Thailand has become a key destination, with Malaysia and Vietnam following closely behind, as firms aim to serve both local and multinational manufacturers expanding in the region.

Renewable Energy Equipment

China’s investments in renewable energy equipment in ASEAN predominantly focus on solar photovoltaic (PV) and inputs manufacturing. This sector’s dynamics are closely tied to global regulations; Chinese firms started expanding in the mid-2010s, responding to U.S. and EU trade barriers that imposed high duties on solar panels. Vietnam has become a focal point for these investments, capturing approximately half of the total value yearly since 2016.

Chinese solar PV investments surged in 2020, influenced by U.S. regulatory actions. Although duties were suspended to tackle inflation for panels sold in the U.S., Chinese firms anticipated their reinstatement, leading to increased local content production in Cambodia, Malaysia, and Vietnam. In 2023, substantial investments from firms like Trina Solar and JA Solar Technologies were announced to expand manufacturing capacity in Vietnam, while production was redirected to avoid penalties from moving operations out of jurisdictions facing higher duties.

Automotives

Automobile manufacturing has consistently been a key focus for Chinese FDI in ASEAN, particularly in terms of transaction numbers. The value of these investments has surged since 2021, predominantly manifesting through greenfield projects alongside a few notable M&A transactions. Investments have spanned nearly all segments of the automotive supply chain.

Countries like Thailand, Vietnam, and Cambodia have attracted numerous auto parts plants, notably in electronics with PCBs, while vehicle assembly remained concentrated in larger markets like Indonesia and Thailand, facilitated by state-owned enterprises. Recently, a wave of electric vehicle (EV) manufacturing plants has emerged across these markets, driven by private Chinese companies such as BYD and Geely, capitalizing on local demands.

Indonesia, buoyed by stringent export policies on critical raw materials like nickel, has catalyzed substantial investments, fostering a more comprehensive supply chain from raw material processing to battery manufacturing. From 2022 to 2023, nearly half of Chinese automotive investments poured into Indonesia, showcasing the region’s growth potential.

Outlook

U.S. tariffs initiated in 2017 have been pivotal in driving Chinese firms’ manufacturing FDI into ASEAN. Continued high tariff rates are anticipated to spur further diversification among Chinese companies. Following the inauguration of President Trump in 2025, tariffs on China surged dramatically, likely sustaining pressure for companies to maintain a presence in ASEAN to access U.S. markets.

Three critical factors will determine the trajectory of Chinese FDI in ASEAN. First, the disparity in tariffs between ASEAN and China will play a significant role; if the gap remains substantial, the region will continue to attract Chinese investment. Second, growing U.S. scrutiny over China’s role within ASEAN supply chains may necessitate tighter controls over transactions, altering the competitive landscape for these nations.

Lastly, China’s overall economic performance will impact FDI flows significantly. A downturn in key sectors could diminish outbound investments as companies navigate challenges and efforts to retain manufacturing jobs domestically intensify. This transition reaffirms the necessity for vigilance and strategic planning as both economies continue to evolve within this dynamic landscape.